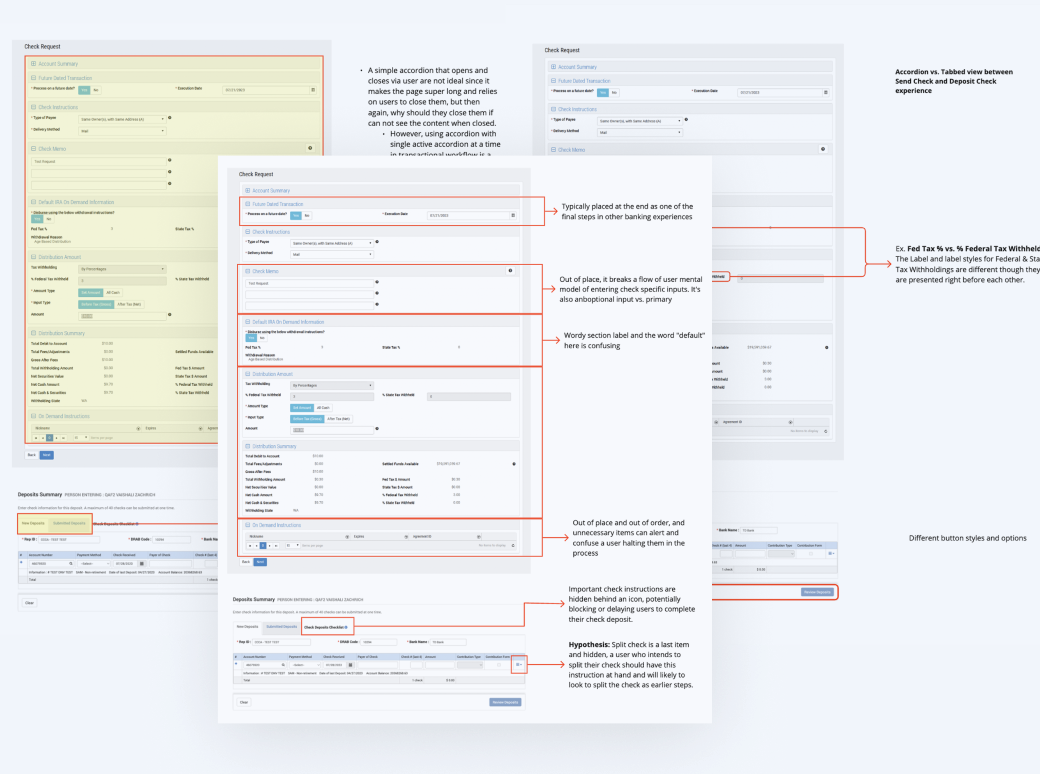

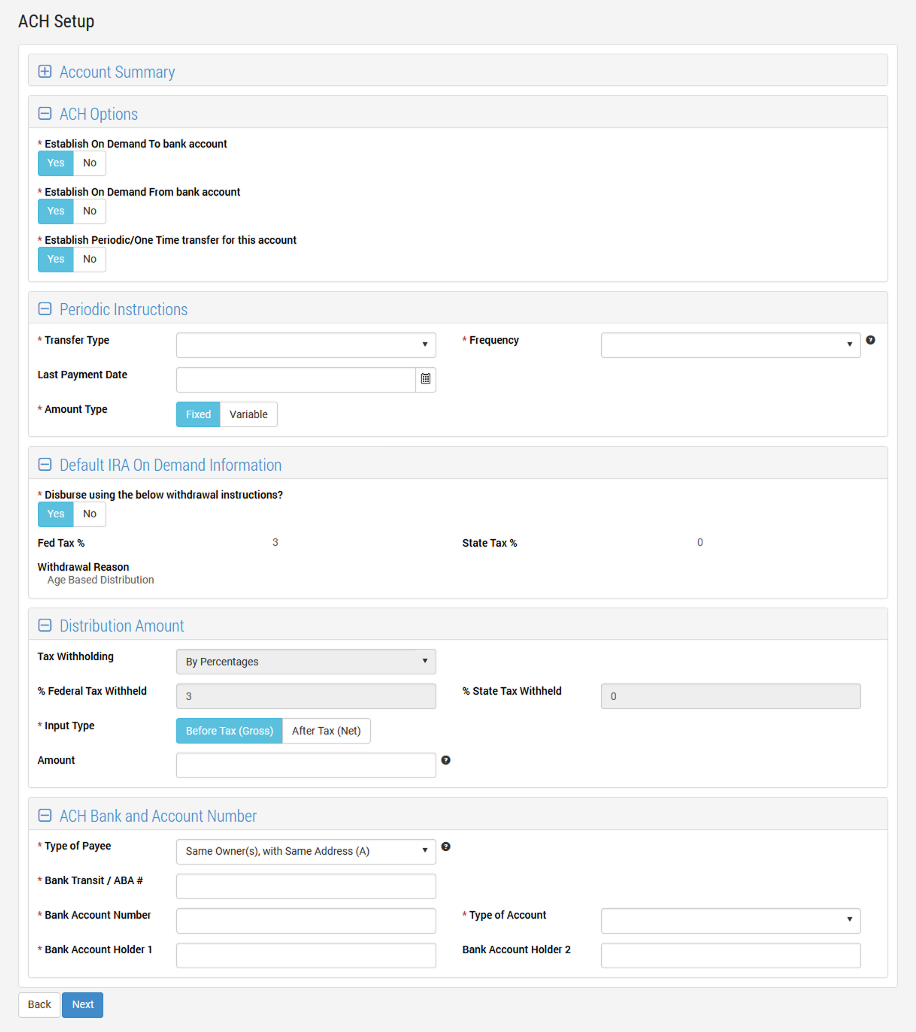

Move Money is primarily used by financial advisors and their administrative staff to execute money transfer requests on behalf of clients. The most common transfers occur between account owners, yet users were unable to save instructions for these recurring transactions, forcing them to re-enter the same information each time. Complex, extraneous content and inadequate form design increased cognitive load and often required users to contact support. When requests resulted in NIGO (Not In Good Order) errors, advisors faced uncertainty around transfer completion, reducing confidence and prompting repeated follow-up until transactions were completed. Ultimately, advisors needed a money transfer experience that was fast, accurate, and dependable—one they could trust with their clients' financial transactions.

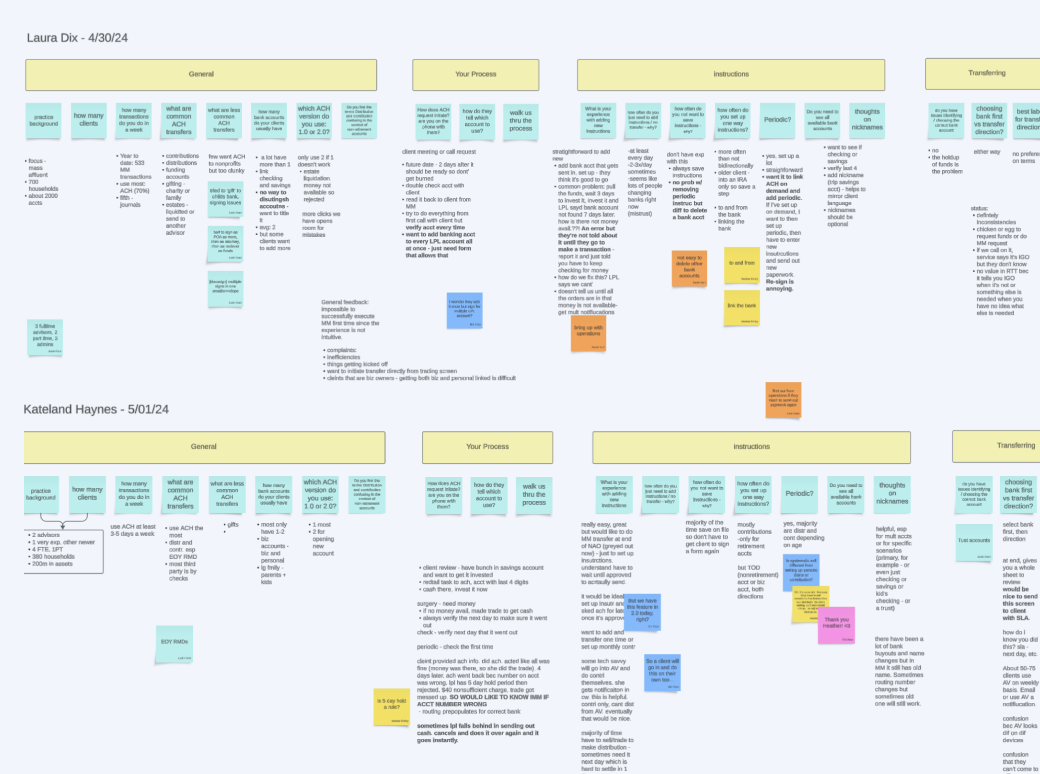

User research methodoloies used: heuristic and data, data flow analysis, user interviews, review and synthesize over 500 user feedback, user journey

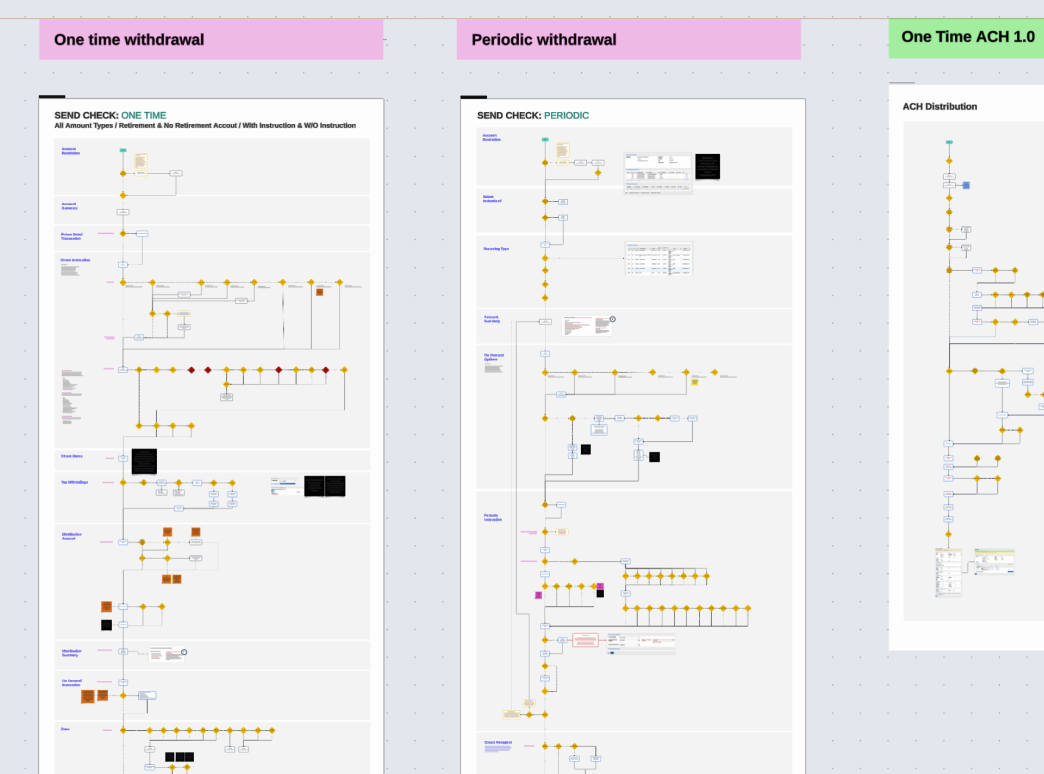

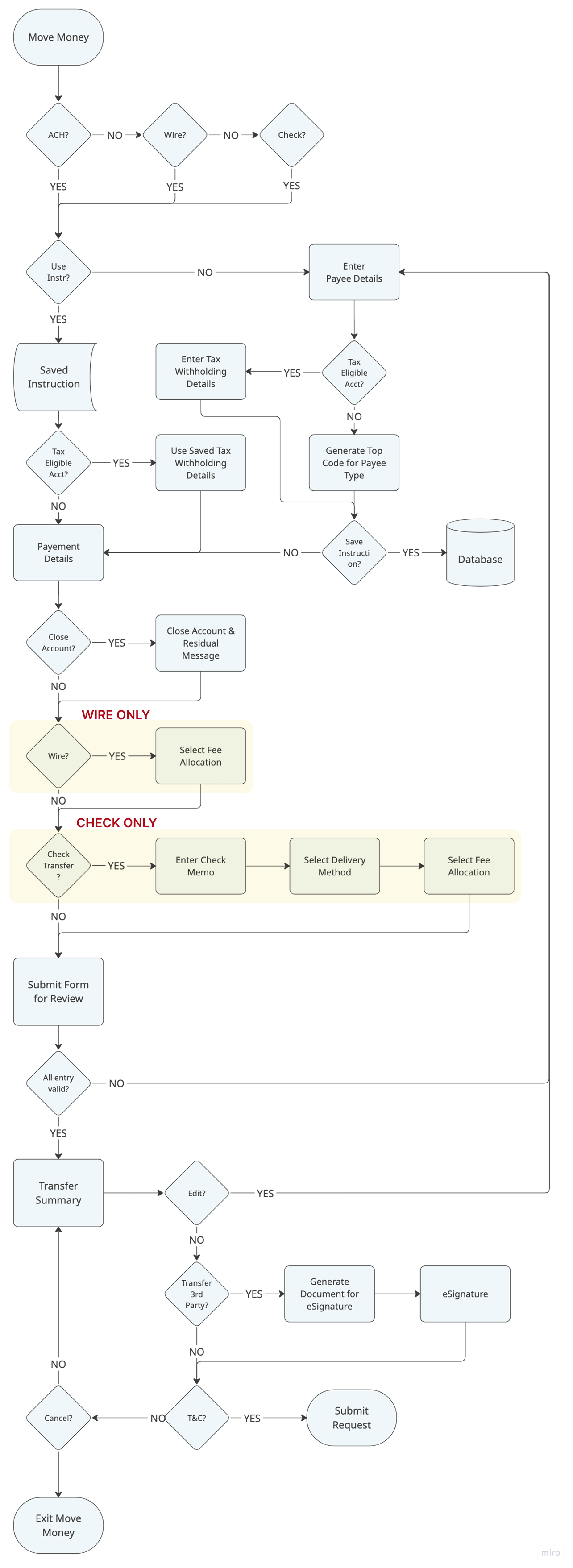

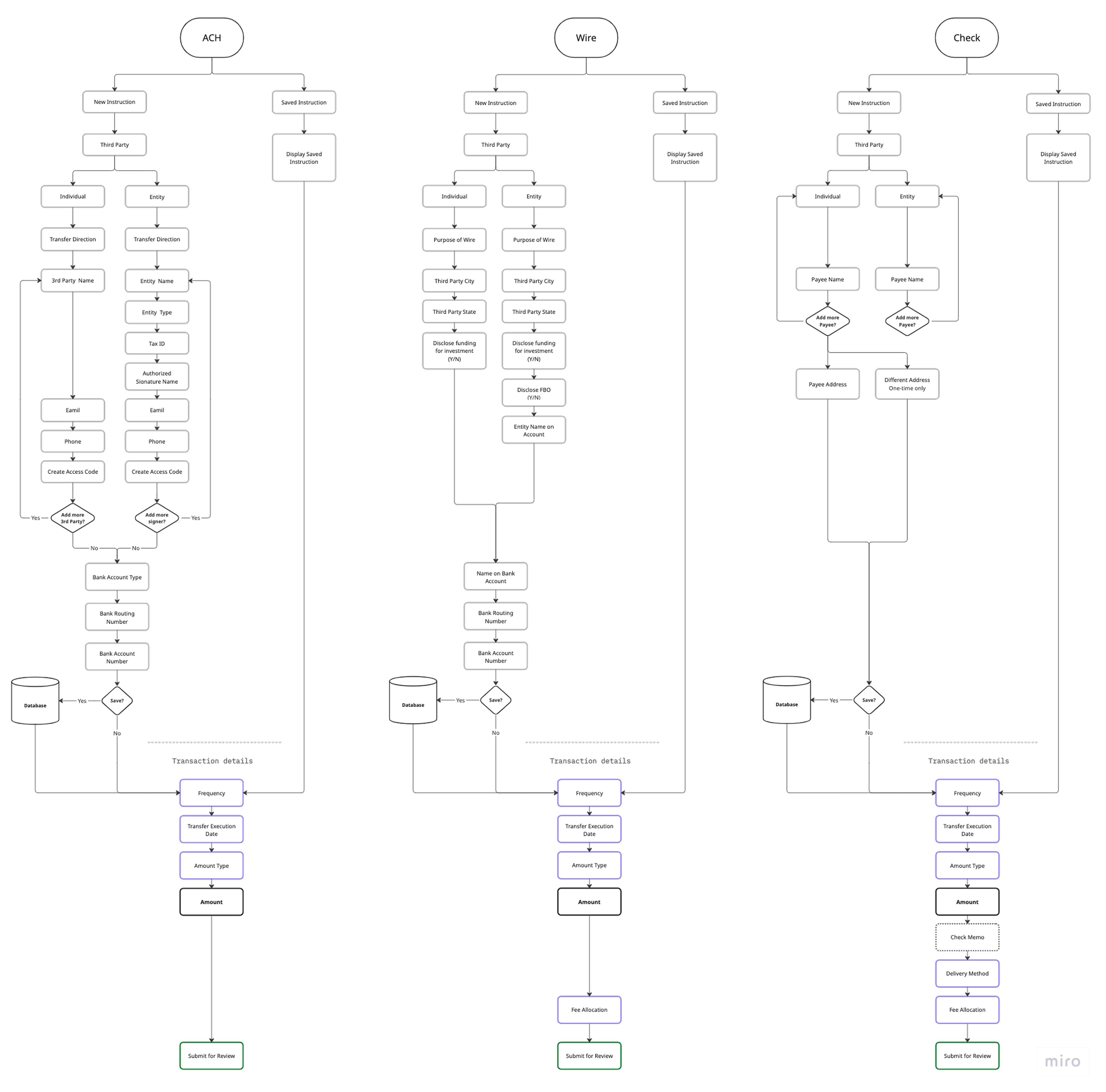

This project began as a redesign of a transfer workflow. It ultimately became the foundation for a unified interaction model that could scale across transfer types while moving operational complexity out of the interface and into the system.

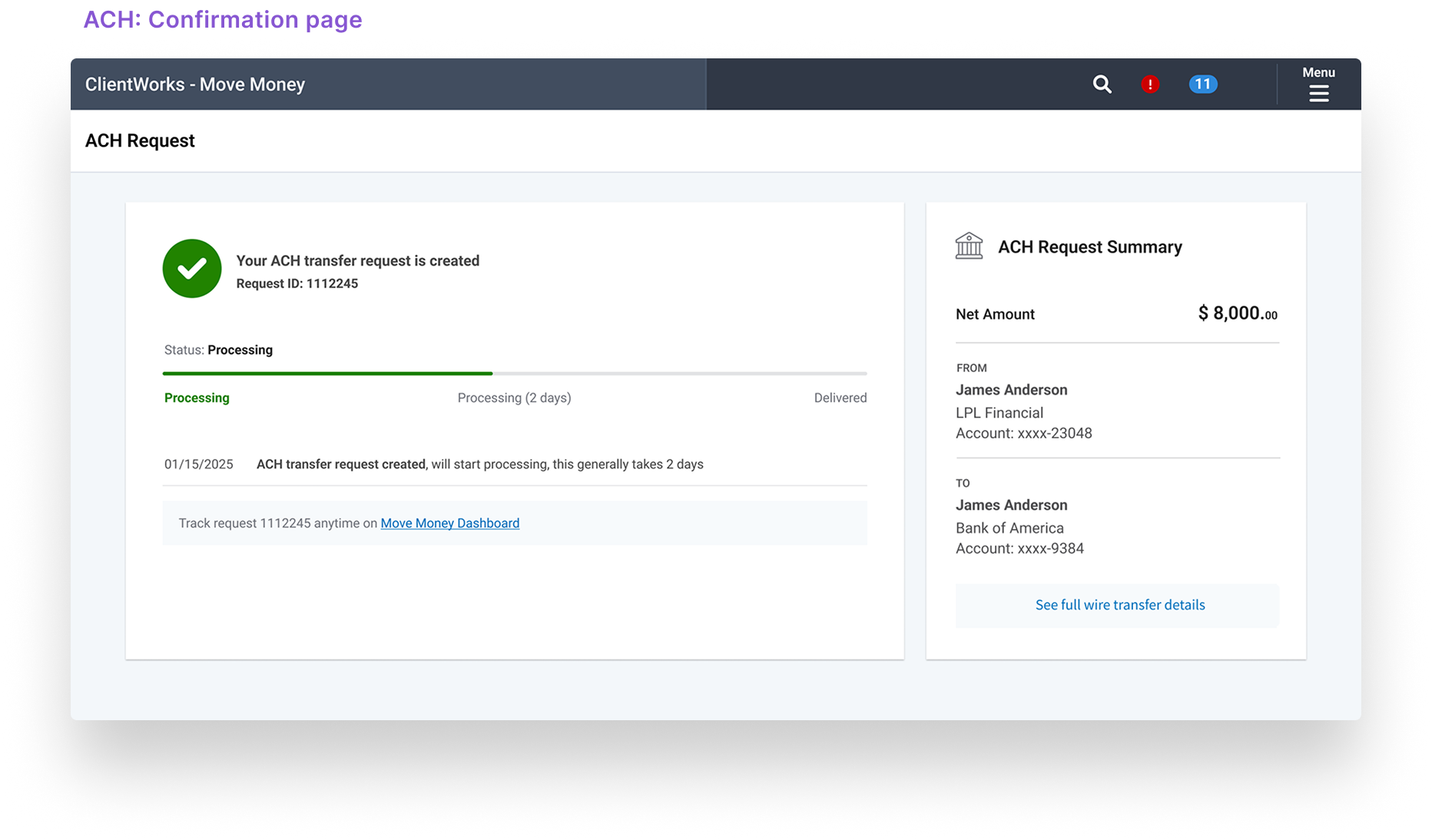

Results reflect the ACH and Check release. Wire launched after the measurement period.

Move Money reinforced several principles that continue to shape how I approach complex enterprise products. Beyond the measurable outcomes, the project reaffirmed the value of questioning assumptions, partnering across disciplines, and grounding product decisions in how people actually work.

The best product ideas are discovered together.

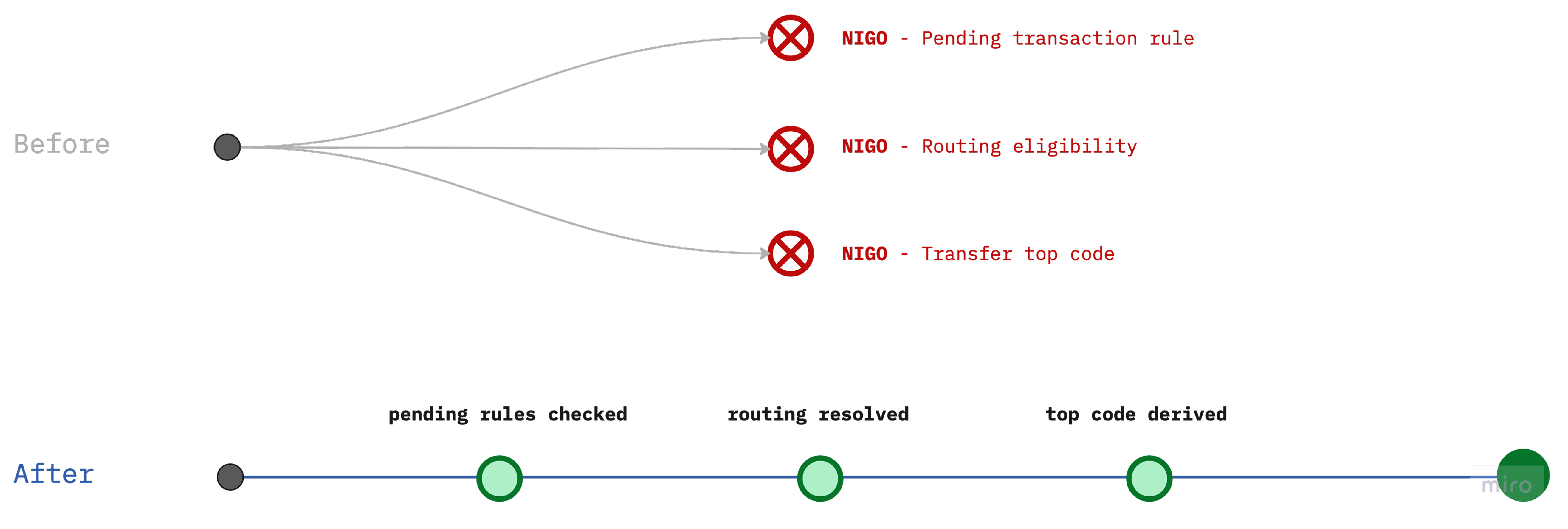

The most valuable design conversations didn't end once requirements were defined. Throughout the project, every constraint became an opportunity to ask, "Why does this exist?" and "Is there another way?" That mindset led to a unified interaction model across transfer types and transformed what initially appeared to be a compliance limitation into one of the product's defining strengths: default account-owner instructions generated from information already on file.

Great enterprise UX is often invisible. Users simply accomplish their task accurately, efficiently, and with confidence because the system quietly carries the complexity for them.

Data should inform product decisions—not make them.

Before the Move Money redesign, the organization invested in a standalone ACH experience because ACH represented more than 90% of transfer volume. Based on the data alone, I likely would have reached the same conclusion. Yet the redesigned ACH experience achieved only about 2% adoption because advisors still relied on the legacy experience for every other transfer type.The experience was a powerful reminder that data is only one part of the story. Understanding users' goals, mental models, and workflows must come before optimizing around metrics. Data tells us where to look. User research tells us what to build.