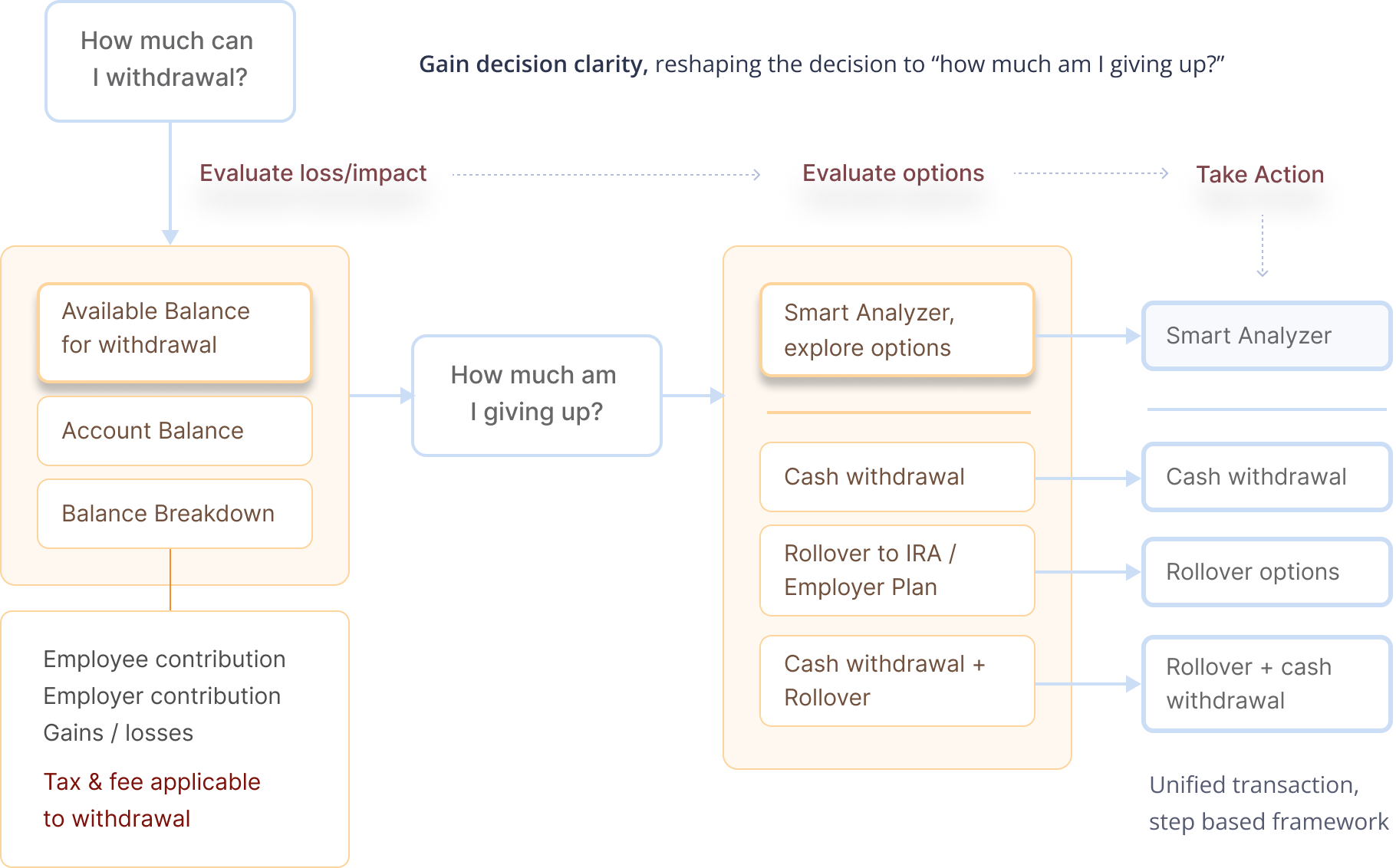

T. Rowe Price managed retirement distributions entirely on paper — a $14M annual process. Users had to call a representative tasked with explaining implications and encouraging reconsideration. But distributions are highly considered decisions. By the time users called, they had already made up their minds. The model created friction for users trying to proceed and put representatives in the position of working against user intent.

T. Rowe Price recognized that this model was costly — both operationally and experientially. Moving distributions online offered an opportunity to reduce costs, respect user autonomy, and shift the experience from persuasion to informed decision-making. Terminated participants — those leaving employer-sponsored plans — accounted for 60% of total distribution costs, making them the natural starting point for the first online MVP. What began as a cost-reduction initiative became an opportunity to redefine how a retirement institution supports participants at one of the most financially significant moments of their lives.